Author: David Martinez, Tax Attorney, PEO Structure Specialist

Publication Date: April 22, 2026

Disclaimer: This article provides educational information comparing retirement account planning with healthcare premium tax treatment. It is not tax advice, legal advice, or insurance advice. Tax strategy, retirement account eligibility, and health plan access vary by individual circumstance, business structure, state, and year. Before making structural changes to your business, consult with a CPA, tax attorney, or licensed professional. USA Ops is an independent referral partner connecting qualified businesses to PEO services. We do not underwrite, enroll, quote, or guarantee insurance.

The Retirement Article That Misses the Bigger Tax Problem

Charles Schwab recently published a comprehensive guide titled “8 Key Facts About IRA Rules” that thoroughly explains how traditional and Roth IRAs work, contribution limits, income phase-outs, and withdrawal strategies.

It’s a solid article. Schwab is authoritative on retirement accounts. They understand 401(k)s, IRAs, and the mechanics of tax-deferred savings.

But if you’re earning $100,000 to $300,000 as a self-employed business owner, Schwab’s article answers only half of your tax optimization problem. And worse—it points you toward a solution that doesn’t fully apply to you.

Here’s why.

Schwab’s Own Numbers Prove the Point

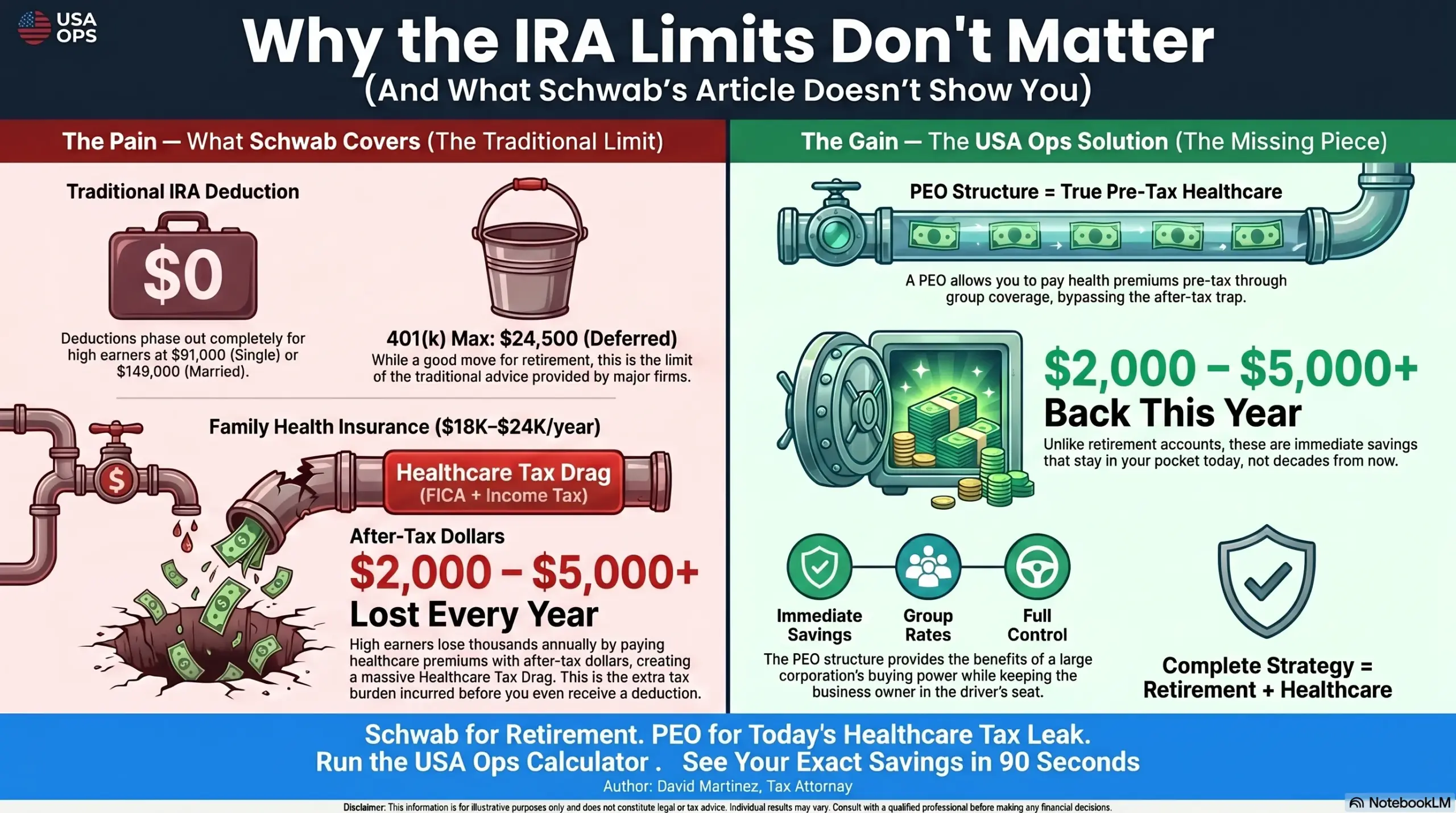

According to Schwab’s article, for a single filer, the traditional IRA deduction is completely phased out at a Modified Adjusted Gross Income (MAGI) of $91,000. For married couples filing jointly with one spouse in a workplace retirement plan, the phase-out ends at MAGI of $149,000.

If you’re reading this and you’re earning $100,000 to $300,000 net, your MAGI puts you well above both thresholds.

What Schwab doesn’t emphasize: You can’t deduct a traditional IRA contribution at all.

You can still contribute to a Roth IRA (with income limits), or you can contribute to a 401(k) (no income limits). But the traditional IRA deduction that Schwab spends considerable space explaining? It’s unavailable to you.

Schwab’s article is technically correct for everyone. It’s just not practically useful for high earners.

The Incomplete Picture: What Schwab Covers vs. What It Misses

What Schwab’s Article Does Cover

✓ How traditional and Roth IRAs work

✓ Contribution limits and income phase-outs

✓ Tax deductibility rules for traditional IRA contributions

✓ Withdrawal rules and required minimum distributions (RMDs)

✓ Beneficiary rules and inheritance mechanics

✓ Comparison with employer-sponsored retirement plans

For your income level: The practical takeaway is simple—max out your 401(k) at $23,500/year and use a Roth IRA if you’re still under the phase-out limits. The traditional IRA deduction is not available to you.

What Schwab’s Article Doesn’t Address

✗ How to reduce the tax you’re paying on your healthcare costs today

✗ Why your family’s health insurance premium is costing you more in gross income than the premium amount itself

✗ The structural difference between an after-tax deduction (like S-Corp health insurance) and a true pre-tax benefit

✗ How high earners can legally access group healthcare pricing and payroll-level tax treatment

✗ The immediate, quantifiable tax savings available outside of retirement accounts

Because Schwab is an investment and brokerage company, their focus is on future tax-deferred wealth building—IRAs, 401(k)s, and where your investment dollars go.

They don’t address current-year cost reduction—how to shield your healthcare premiums from tax before taxes are calculated.

These are two completely different tax strategies solving two completely different problems.

The Real Tax Leak for High Earners: Not Retirement Savings, But Healthcare Costs

Let’s say you’re a $200,000 net income business owner. Schwab’s article advises you to:

- Max out your 401(k) at $23,500/year (tax-deferred)

- Open a Roth IRA if eligible (tax-free growth, but limited contribution)

- Consider a SEP-IRA or Solo 401(k) if self-employed (yes, but still subject to income limits for deductions)

All solid advice. But here’s what it misses:

Your family health insurance is likely costing $18,000 to $24,000 per year. And you’re probably paying for it with after-tax dollars.

According to IRS Publication 15-B, if you own an S-Corporation and pay your health insurance premium, that premium gets added to your W-2 wages (Box 1). You then deduct it as a self-employed health insurance deduction on your personal tax return.

But here’s the trap: The premium was already taxed as income and subject to self-employment tax before you got to deduct it. You’re getting an after-tax deduction, not a true pre-tax benefit.

For an $18,000 annual family premium, this structural inefficiency costs you approximately $2,754 per year in permanent self-employment tax loss—money that never comes back, even with the deduction.

If your family premium is $24,000, that’s $3,672 per year in dead tax.

Schwab’s article doesn’t mention this at all. Because they don’t sell solutions to healthcare cost reduction—they sell retirement investment accounts.

Why These Strategies Should Be Complementary, Not Competitive

You should absolutely follow Schwab’s advice. Max your 401(k). Consider your Roth options. Plan for long-term wealth.

But you’re leaving thousands of dollars on the table if you stop there.

A complete tax optimization strategy for your income level should address:

- Retirement savings (Schwab’s domain): $23,500/year 401(k) contribution + Roth options

- Healthcare cost reduction (the gap): Eliminate the $2,000–$5,000 annual tax leak on your family’s healthcare premium

These work together, not against each other.

How the Structural Difference Works

Schwab’s Retirement Focus (Deferred Tax Savings)

| Strategy | Mechanism | Benefit | Timing |

|---|---|---|---|

| Traditional 401(k) | Contribute $23,500 pre-tax | Reduce current-year taxable income | Deferred (taxes due on withdrawal in retirement) |

| Roth IRA | Contribute $7,000 after-tax | Tax-free growth and tax-free withdrawals | Deferred (benefit realized in retirement) |

| Solo 401(k) (self-employed) | Contribute up to $69,000 (with employer match) | Larger tax shelter for high earners | Deferred |

Common trait: All reduce taxes in the future, not the present year (except for the income deduction itself).

The Missing Strategy (Immediate Tax Savings)

| Strategy | Mechanism | Benefit | Timing |

|---|---|---|---|

| PEO group coverage via payroll | Healthcare premium deducted pre-payroll | Eliminate FICA and FIT on the premium amount | Immediate (this tax year) |

Key difference: This saves taxes today, not “when you retire.”

For a $200,000 income owner with an $18,000 annual family premium:

- Schwab’s strategies save you approximately $5,640/year in deferred taxes (on the $23,500 401(k) contribution at 24% marginal rate)

- Healthcare pre-tax strategy saves you approximately $2,754/year in immediate taxes (on the $18,000 premium that currently leaks to FICA)

- Combined: You save roughly $8,400 in total tax burden (some deferred, some immediate)

Schwab covers the first part. The second part—the immediate healthcare savings—is what this article addresses.

The Calculator: Where Schwab’s Article Leaves Off

Run the calculator to see exactly how much of your current gross income is being lost to the structural inefficiency of paying healthcare premiums with after-tax dollars.

Enter:

- Your net business income

- Your annual family health insurance premium

- Your filing status

The calculator will show you:

- How much gross income you need to fund your current healthcare cost (after-tax method)

- How much gross income you’d need if the premium were pre-tax (PEO structure)

- Your annual savings potential

- Your monthly savings potential

Most business owners earning $100,000–$300,000 discover they’re leaving $2,000 to $5,000 per year on the table due to the healthcare tax inefficiency—money that has nothing to do with retirement account contributions.

What This Means for Your Tax Strategy

Schwab’s advice is incomplete, not wrong. For high earners, it should be part of a broader tax optimization plan that also addresses:

- Immediate healthcare cost reduction (what this article addresses)

- Future retirement savings (what Schwab addresses)

- Payroll tax optimization (structure-dependent)

- State-specific tax considerations (varies by where you operate)

Schwab doesn’t cover #1 because they’re not in the business of healthcare cost optimization or PEO structures. They’re focused on retirement accounts and investments.

That’s a gap worth filling.

Who This Matters Most To

S-Corporation owners earning $100,000–$300,000 with family healthcare premiums

Single-member LLCs taxed as S-Corps with similar income

High-income professionals (physicians, attorneys, consultants) operating as solo or small partnerships

Multi-owner S-Corps where multiple owners are each taking health insurance premiums

If Schwab’s income thresholds disqualify you from traditional IRA deductions, you’re exactly the person who benefits most from addressing the healthcare cost structure that Schwab doesn’t mention.

How to Get Started

Step 1: Understand the gap

Run the calculator and see exactly how much your current structure is costing you on healthcare alone.

Step 2: Ask the right questions

If the number is material (more than $1,500 per year), it’s worth a conversation with your CPA about whether a PEO structure makes sense for your situation.

Step 3: Build your complete tax strategy

Combine Schwab’s retirement account optimization with healthcare cost reduction for a comprehensive plan.

The Bottom Line

Schwab’s retirement article is authoritative and thorough—for retirement accounts.

But if you’re a high earner, it leaves your most significant current-year tax leak completely unaddressed: the structural inefficiency of paying healthcare premiums with after-tax dollars.

That’s not a criticism of Schwab. It’s a gap in their domain of expertise.

This article fills that gap by showing you exactly how much you’re losing and providing a calculator that quantifies your specific situation.

Sources and Disclaimers

Official References:

- Charles Schwab IRA Rules Guide (cited throughout)

- IRS Publication 15-B — Fringe Benefits

- IRS Topic 502 — Medical and Dental Expenses

- IRS Publication 590 — Individual Retirement Arrangements

- IRS Section 162(l) — Self-Employed Health Insurance Deduction

Educational Disclaimer:

This article compares the scope of Schwab’s IRA guide with the gap in healthcare cost optimization for high earners. It does not constitute tax advice, legal advice, or insurance advice. Schwab’s article is factually accurate within its domain (retirement accounts). This article expands the domain to include healthcare cost structures.

Tax treatment, retirement account eligibility, healthcare cost optimization, and PEO structures vary by individual circumstance, business entity type, state, and year. Before making structural changes, consult with a licensed CPA, tax attorney, or other qualified professional.

USA Ops is an independent referral partner. We do not underwrite, enroll, quote, or guarantee insurance. PEO services are provided by certified employers; we connect qualified businesses to those services.

About the Author

David Martinez is a tax attorney specializing in business structure optimization and PEO implementation for high-earning solo professionals and small business owners. With 14 years of experience in tax law and corporate strategy, David focuses on identifying structural inefficiencies that mainstream financial advisors overlook. He regularly works with CPAs, business coaches, and fractional CFOs to help clients redesign their tax and benefits strategy after major income shifts or business growth events.

David holds a Juris Doctor from the University of Michigan Law School and has contributed to articles in Tax Advisor Magazine and The American Bar Association Journal. He is licensed to practice law in seven states and frequently speaks at business owner conferences on S-Corp optimization and alternative benefit structures.

His specialty is identifying what conventional financial institutions don’t address—the gaps between standard business advice and the actual mechanics of tax law that create opportunities for high-income owners.